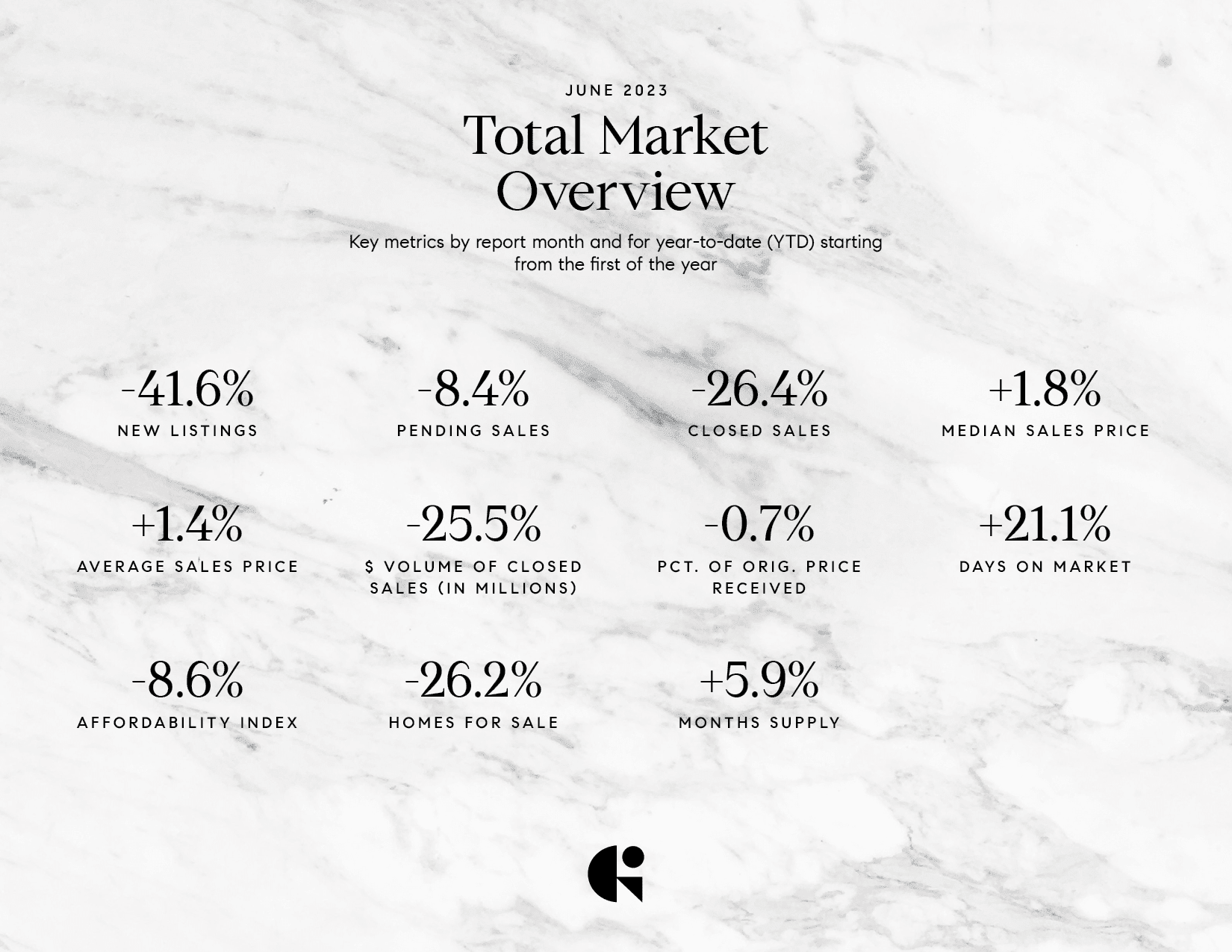

JUNE 2023

Low inventory and higher borrowing costs cool US housing market despite rising temperatures. Existing-home sales down 20.4% YoY. Closed and pending sales decline. Median prices see slight increase. Days on market and supply show mixed changes. Nationwide inventory increases, but shortage persists. Prices remain high, but with a 3.1% decline YoY. Demand exceeds supply, leading to quick property sales.

For the full Monthly Indicators Click Here

San Diego County (CA)

Lost $550.60 million in annual AGI*

Wealth Migration 1992-2021

Gained Wealth From:

| $2.76 billion |

Los Angeles County, CA |

| $1.35 billion |

Orange County, CA |

| $932.01 million |

Santa Clara County, CA |

| $598.41 million |

Cook County, IL |

| $509.26 million |

San Mateo County, CA |

Lost Wealth To:

| $3.23 billion |

Riverside County, CA |

| $1.12 million |

Clark County, NV |

| $569.49 million |

Maricopa County, AZ |

| $272.75 million |

Travis County, TX |

| $259.93 million |

Yavapai County, AZ |

3 Reasons Why A Recession Is Still Likely

......followed by.......

"The sharply reduced inflation rate is promising, yet core inflation remains closer to 5%. Here are some thoughts as to why this economy might contract still as rates get raised too far, too fast....and are raised again soon:

1. COST OF AND ACCESS TO CAPITAL:

"These rapid rate hikes that have occurred at unprecedented speed have put my small businesses - companies with 5 to 500 employees, which represent over 60% of our economy - in a bind. If you're in the S&P 500, you have no trouble financing your business. You can't say that about small business anymore. The cost of capital has gone through the roof." - Kevin O' Leary. Not to mention access to capital....yes, even for the wealthy.

2. RISING DEBT - YOLO (You Only Live Once, buy now pay later) consumers:

Have you noticed all those Instagram posts of worldwide travelers, especially those travelling in (expensive) Europe to re-create their own 'White Lotus' experience? Many can afford it, but most are spending on credit cards. Those credit card debts are mounting.....at much higher - and rising - interest rates. And soon those debts will come due. Debt service is MUCH more expensive than a year ago. Households added $148 billion in overall debt, bringing the total to $17.05 trillion. Balances are now $2.9 trillion higher than just before the pandemic.

3. DWINDLING SAVINGS

Some estimate that excess consumer savings are 'down' to about $500 billion. Once this excess is spent on already more expensive goods that while not rising as quickly in price, are still much higher than 2 years ago, spending cutbacks will become essential for many, and chosen by those with a more conservative fiscal mindset. US consumers amassed about $2.3 trillion in savings between 2020 and mid-2021 (Fed economists), about $2 trillion more than they would have saved under normal circumstances. Estimates place that now closer to $500 billion once you factor in buy-now-pay-later debt that has not registered yet.... and it appears most of this is in the hands of wealthier consumers.

The FED was slow to acknowledge realities around rising inflation because the data they watch has a slow, long lag time. Nothing has changed, so to believe they are looking at more real-time data now might be presumptuous at best. Is there ONE upside to all this? Possibly, yes. Not unlike rising inflation, at one point the FED will realize they have gone too far, too fast and LOWER rates to stimulate the economy back to life.....and because they have gone pretty high, they have more room to make those downward adjustments feel significant enough to make a difference. A brief - and possibly potent - economic pullback is very possible....but then when rates are lowered closer to 5%, buckle up kiddo's.....pent up demand and postponed plans will unlock and a post-Covid, post-9-11 real estate market might ensue....."

By Leonard Steinberg